- Green Rising

- Posts

- 🚁 Heli view: We need to talk about CH4

🚁 Heli view: We need to talk about CH4

Natural gas could be transformative for Africa’s green economy. But its accelerating success must not crush other sustainable sectors.

The main risk is to renewables, green hydrogen and electric mobility.

But first the upside…

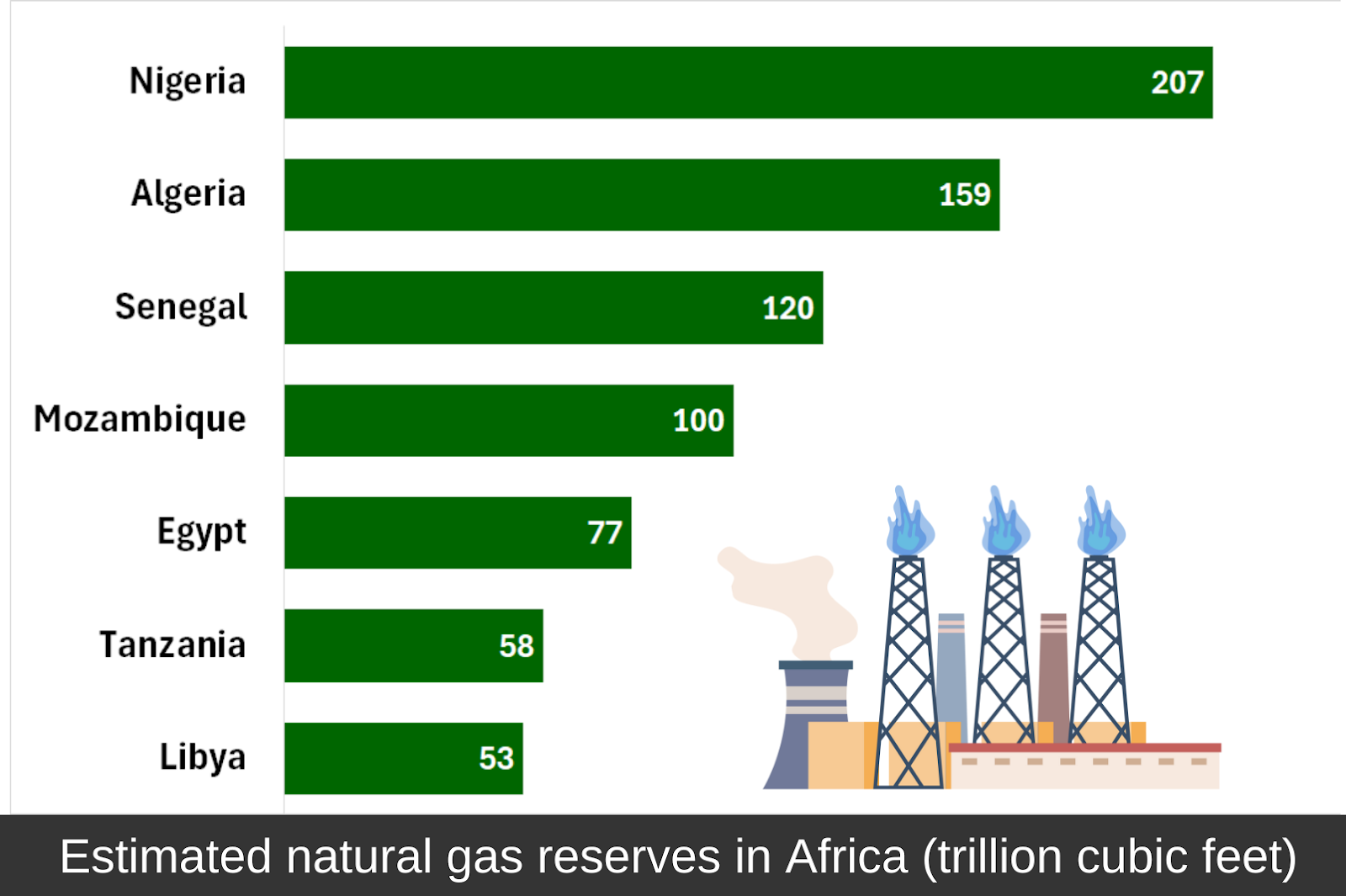

African natural gas accounts for 7.5% of the world's proven reserves.

Nigeria, Algeria, Mozambique and Senegal are the main gas countries.

Extraction has almost doubled since 2000 thanks to new investments.

Cash cow: The continent exports 60% of its gas, generating much needed foreign income.

Algeria has two major intercontinental pipelines that export gas to Europe.

The country earns $15 billion annually. Nigerian gas generates $8 billion.

Going big: Africa's role as a global gas supplier is expected to grow.

Putin push: Demand from Europe is driving new investments in Africa.

Russia's invasion of Ukraine upset EU gas markets and boosted Africa demand.

Europeans buy 90% of the continent’s gas, while being Africa’s top climate funder.

At home: Gas consumption on the continent is small but rising.

Magic juice: More gas use could grow business sectors across Africa.

Gas-based fertilisers boost crop yields, addressing food insecurity.

Compressed Natural Gas (CNG) vehicles reduce reliance on imported diesel.

African governments push gas as a catalyst for industrialisation and jobs.

The champions: To gas advocates in the private sector it is a form of clean energy.

South African miners uses gas to reduce coal dependency and cut emissions.

Nigeria boosts gas use to avoid burning other biomass and reduce deforestation.

Metal processing and cement production substitute gas for diesel to decarbonise.

Tanzania expands the use of gas in cooking to reduce indoor pollution.

The critics: A potential negative impact of natural gas on the environment is clear.

Production in Africa is 80% more carbon-intensive than global averages due to leaks during extraction and transportation.

Nigerian flaring of gas is linked to respiratory illnesses, acid rain and premature deaths in nearby communities.

Coastal gas infrastructure threatens marine ecosystems through habitat disruption and pollution.

Category risk: Gas expansion also means locking Africa into fossil fuel dependency.

Renewables could create more jobs per MWh than gas, even in Nigeria and Senegal.

Gas exports are a volatile economic foundation. Prices are set to fall from 2030.

Investments are made over decades, leaving little flexibility in a transition.

More immediately: The risk is that gas could starve other sustainable sectors of capital.

Unlike gas, newer sectors often still have to prove their economic worth.

In an already tricky investment climate, this could hamper green growth.

Power play: The renewables sector is vulnerable. Gas could undercut its momentum.

Solar and wind energy are making great strides in Africa.

Miners and industrial firms are converting to renewable power systems.

But gas hasn’t given up. In places it may indeed fit alongside renewables.

Latest darling: The green hydrogen sector has recently attracted billion-dollar investments.

Here too gas sees a competitor. Hydrogen as a mass fuel may still be years away.

But success will be harder to achieve if it is replacing gas rather than oil.

Mobility revolution: And might the cars of Africa’s future be powered by compressed natural gas (CNG) rather than electric batteries?

South Africa, Nigeria, Egypt and Tanzania are investing in CNG vehicle conversions.

They say this will cut emissions cheaply and soon – even if by less, which is true.

The danger here is that Africa’s nascent electric vehicle sector loses momentum.

This could impact job creation in vehicle assembly plants just springing up.

Two-track solution: The continent can and should leverage gas for growth – while doubling down on renewables, green hydrogen and electric mobility.

It has little choice but to try and finesse multiple opportunities alongside each other.

Reply